Does iShares SLV ETF Really Hold Silver?

The iShares Silver Trust (SLV) has been the subject of controversy since it first started trading. The objective of the exchange traded fund, according to the iShares website:

Is for the value of the shares of the iShares Silver Trust to reflect, at any given time, the price of silver owned by the iShares Silver Trust at that time, less the iShares Silver Trust's expenses and liabilities.

That is, there's supposed to be a vault somewhere with a bunch of physical silver and each share of the SLV is supposed to represent about an ounce.

Three main parties are responsible for the SLV. The sponsor, iShares, is a subsidiary of BlackRock (BLK). It arranged for the creation of the trust and its listing on the NYSE Arca. It assumes certain marketing and administrative expenses of the trust.

The trustee is Bank of New York Mellon (BK). It is responsible for the day to day administration of the trust, including processing orders, coordinating with the custodian, calculating the net asset value of the trust, and selling the trust's silver to pay for expenses.

The custodian is JPMorgan Chase (JPM). It is responsible for holding the trust's physical silver in its vaults. The prospectus states that JPM:

Is responsible to the trustee [Bank of New York] only. Because the holders of iShares are not parties to the custodian agreement, their claims against the custodian may be limited.

Interesting.

The controversy is whether there is a vault that actually contains the amount of silver iShares says it does. Mainstream media hasn't weighed in on one side or another, but the blogosphere and Youtube are full of various accusations and speculation.

An interesting thing happened a day or so ago. According to Zero Hedge, Kevin Feldman, managing director of iShares, issued arefutation of the rumors that the SLV contains no physical silver.

This reminds me of the CEOs of Bear Stearns and Lehman Brothers saying everything is fine shortly before their banks collapsed. It's also reminiscent of the other Wall Street CEOs saying everything was great and they didn't need to borrow any money while they were borrowing billions and teetering on the edge of insolvency. It also brings to mind the often quoted phrase, "never believe anything until it's been officially denied."

People are suspicious of the SLV for a number of reasons. Here are two.

First, there is a silver shortage. Eric Sprott, who runs, among other things, a physical silver fund (PSLV), has commented often in the recent past on how hard it is to buy physical silver in large amounts. Various mints, including the US Mint, are also unable to get sufficient supplies.

Second, the silver shortage has caused premiums for the physical metal to skyrocket. Sprott's fund has traded in recent days at about a 20% premium to the spot price. Silver coins at shops like the American Precious Metals exchange sell for a premium of over 9%.

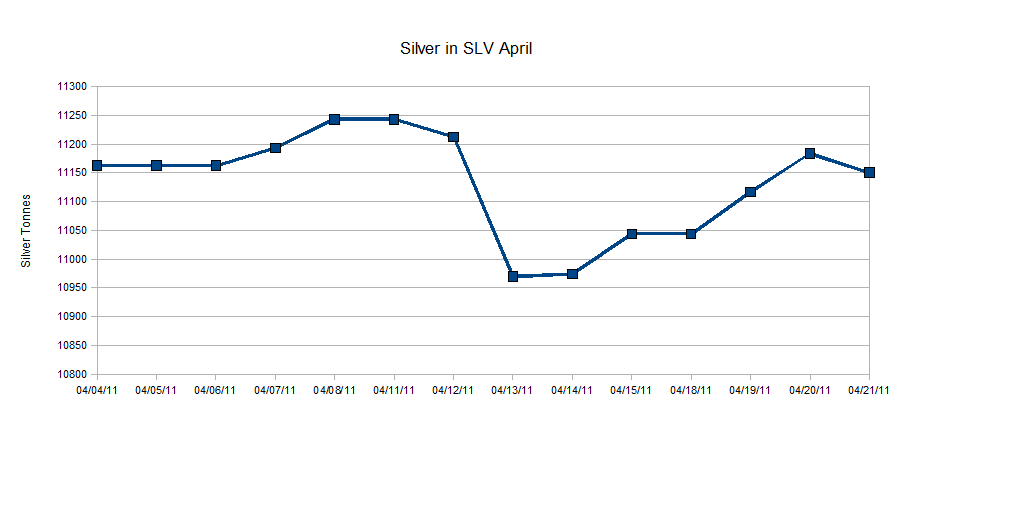

Add these two together and it seems really weird that the SLV can increase and reduce its silver holdings daily seemingly with no trouble. For example, they decreased their holdings by 33 metric tons onThursday.

All the data is available on the iShares website in the left hand column. Here is a chart of the trust's silver holdings since the start of April (click to enlarge):

How is it possible for the SLV to buy and sell such large quantities of silver on a daily basis when no one else, it seems, can do so? It's expensive to procure physical silver, and usually takes much longer than a day. Transportation costs would presumably also present a problem.

According to the Inspection of Silver Bullion document on the SLV website (dated July 2010), there are two vaults operated by JPM, two vaults operated by Brinks Global Services, and one vault operated by Via Mat International. That makes five vaults in total with subcustodians operating three. What comes to mind is guys with forklifts moving bullion from one part of a warehouse to another, into the account of another silver market participant. So, for example, when the SLV dumped 33 metric tons of silver the other day, guys on forklifts in one or more warehouses moved the silver from Bank of New York Mellon's account to the accounts of whoever bought it.

The portion of the SLV prospectus that deals with the custodian seems to suggest that this is what takes place. (I say seems because I read it a number of times and am still not quite sure I understand it. It's among the more convoluted things I've read in my life, and I'm a law school graduate. I doubt that the obfuscation in the prospectus is accidental.)

But another question arises. How are buyers and sellers so readily available daily? Buyers at the moment are not a problem, given that there is a shortage. Sellers, on the other hand, are presumably hard to come by. (Maybe the custodian deposits the silver into its own accounts and then sells it back to the trust? I'd like to know.)

Moreover, can the prospectus and inspection certificate be trusted? Banks are not generally regarded as the most honest businesses, as one scandal after another has shown.

Banks have a particularly sordid history with silver. Here are a couple of recent examples.

There's currently a class action lawsuit against UBS that alleges the bank sold investors phantom silver. The plaintiff alleges that he bought silver bars from UBS, paying the bank monthly storage fees. After a while he decided to store the bars himself and demanded delivery of the metal. UBS didn't comply. After a series of ever more frustrating queries, plaintiff finally learned that UBS never purchased silver bars for him. The bank eventually responded, in a purposefully confusing letter, that he would have to sell his current "unallocated position" and buy "a silver position," at additional expense. So the plaintiff paid storage fees for no reason at all. And all that time the bank had apparently led him to believe that he had "a silver position," that is, specific silver bars segregated for him in a vault.

In 2007, Morgan Stanley (MS) agreed to pay $4.4 million dollars to settle a suit that alleged a similar scheme. In that case Morgan Stanley claimed that it followed industry practices. It has beensuggested that "banks are in the habit of keeping only 1 bar for every hundred that are supposed to be in their vaults." If it's industry practice to make investors believe they're purchasing physical silver when in fact they are not, it is conceivable that the same sort of thing is involved in SLV. Given that JPMorgan, the custodian of the silver in SLV, has been investigated for silver manipulation I would say that more than conceivable, it is likely. How many claims are there on the allocated bars in the five vaults?

So, to summarize, there have been rumors and questions about the SLV's silver holdings. A banker from BlackRock took the time to officially deny these rumors. That's suspicious. The SLV prospectus in its vague language suggests that there is actual physical silver owned by the trust. It also answers, sort of, some of the questions regarding how such vast amounts of silver are bought and sold daily while other market participants have to wait weeks and months for delivery. But bankers have historically not been very honest people in general and their recent activities with silver do nothing to assuage people's suspicions.

Since BlackRock's official denial will most likely backfire, instead of directing investors to the prospectus, Mr. Feldman should answer some of the more practical questions that people have in simple language.

Disclosure: Long physical silver.

All information on this website is for educational purposes only and is not intended to provide financial advise. Any statements about profits or income, expressed or implied, does not represent a guarantee. Your actual trading may result in losses as no trading system is guaranteed. You accept full responsibilities for your actions, trades, profit or loss, and agree to hold MinKL Invest harmless in any and all ways.

No comments:

Post a Comment