The Fraying European Union After a tragic history of bloody wars, Europeans have looked for decades with great hope at the transcendent aspirations of continental cooperation, a European Union aiming to improve relations, enhance trade and prosperity, and prevent future wars. In such a fraternal climate, one might think that the union, as an organization of diverse states, would provide clarity in regard to the financial risks as well as rewards involved in its activities. Unfortunately, it’s not happening. The European Union and European banking system is melting down. In our opinion that’s because the bureaucrats who run it, and who are paid richly to do so, are loath to upset the all-for-one, one-for-all ideal and talk straight to the people. To talk about risks is risky. Better to promote the rosy rewards of togetherness. The EU bureaucrats are far from transparent in disclosing risks to the European public. We point especially to the risks involved with owning the bonds of a number of the nations of the community. In our opinion, the finances of Greece, Portugal, Spain, Italy and Ireland, to name but a few, are on shaky ground. They have been poorly managed. It appears now that the three major rating agencies are beginning to share our views. You may recall several years ago our reaction to assessments by Moody's, Fitch, and Standard & Poors, the major rating agencies, in regard to the risks of some of the mortgage securities that they rated. Clearly over-optimistic, we said. Securities were being labeled as safe or even very safe not long before they collapsed in price as the mortgages and other assets backing them shrunk in value. These inaccurate risk calculations had devastating consequences that threatened the banking systems of the U.S. and Europe, and cost taxpayers trillions of dollars. More recently, the rating agencies have become more realistic and begun identifying problems before bonds in question actually collapse in price. They have lowered ratings on the sovereign debt of over-levered and poorly managed countries (mentioned above). These more honest and realistic assessments are great news for investors and the public at large. The bottom line is that Portuguese, Greek, Irish, Italian, Belgian and Spanish bonds are low quality investments. They deserve to be downgraded, as has now occurred with Portuguese and Irish bonds. For a detailed report from the Financial Times on this significant development, go to or click hereFinancial Times Article The EU’s financial hierarchy, fearful of the consequences, is switching into attack mode against the messengers of bad news. Already officials have issued threats to bar the rating agencies from ranking countries rescued in internationally agreed upon deals. Trying to gag the truth and manipulate the bond markets is fraudulent and deserves to be condemned. Such activity is potentially harmful to the people of Europe and to investors in general. Clearly the markets understand what the bureaucrats are up to and have wasted no time in demanding higher interest rates from the poorly managed countries. Following in the Footsteps of Japan... The U.S. banking crisis of 2008 was by no means a first-of-its-kind. The most immediate previous example was in Japan in 1990, a crisis that generated a long-term economic malaise. Now, the U.S. and Europe are following precisely in Japan’s ill-fated footsteps. Twenty-one years ago Japan’s real estate bubble popped. Property prices fell. Many banks were stuck with bad debts on properties that could not be sold for enough money to repay the loans. Instead of foreclosing and writing off the uncollectable part of the debt, Japanese banks engaged in a process of “extend and pretend.” They loaned money to the borrowers to pay interest. The hope was that property values would revive and therefore the debt could be repaid. This still hasn’t happened! But the banks continue to support “zombie loans” and the system has slowed to a feeble crawl. Banks have no new money to lend because they are too busy extending old loans that will never be repaid. In 2008, the U.S. experienced its own banking crisis after a burst real estate bubble. Banks were bailed out with a transfusion of government money. Most major banks were spared bankruptcy and even the need to fully write off bad debts and recapitalize. Moreover, the practice of creating and selling dubious derivatives that helped trigger the crisis was never stopped. It continues to this day, without transparency, and without a clearing agency to create and oversee standards. Doing business as before permits excess leverage and continued risk for the U.S. banking system. Like the Japanese banks before them, American banks are not liquid enough to lend and take the risks needed to create strong economic growth. Bad loans that have not been written off continue to plague them. Washington is further exacerbating the problem by becoming more restrictive and risk averse, and by erecting barriers to entrepreneurial activity and new company formation. The government evidently does not realize that most new jobs created in the U.S. come from entrepreneurial companies of 50 employees or less. As a result we expect to see continuing economic and growth struggle in the U.S. economy. Today, U.S. companies do not borrow to expand and U.S. banks do not easily lend. U.S. unemployment is stuck at record high levels and ever-rising budget deficits plague the nation. Across the Atlantic, European banks are holding massive exposure to the sovereign debt of ailing nations. Much of this debt may never be fully repaid and investors are starting to realize that European banks are becoming increasingly unstable. The banks are looking more and more like their Japanese and U.S. counterparts. European economic growth is slow and getting slower. The EU is in danger of losing member states that will not be able to meet demands for austerity. We fully expect the EU to experience a partial collapse as Greece and others exit the Euro. The solution is to allow defaults write off bad debt and recapitalize banks. This will not happen. …Japan has suffered for 21 years; how long will the U.S. and Europe let their problem fester? The Japanese government chose a rehabilitation path via infrastructure spending and liquidity. The result, however, has been more government deficits without encouraging long-term growth. The U.S. government has chosen a path via banking liquidity measures and general liquidity — quantitative easing (QE). It has pumped big bucks into the system. The result: some recovery that is now sputtering. The liquidity of QE was important to keep the banking system from imploding and bringing down the whole economy into a deep depression. The liquidity is now in the system and finding its way into commodity prices that are on the rise. Unfortunately, Washington has not learned from Tokyo’s mistakes. The U.S. has emphasized infrastructure repair projects and bad loan bailouts, but it has not created the necessary environment to stimulate entrepreneurial growth which, in turn, creates jobs. This dependence on government-sponsored projects — instead of unleashing the entrepreneurial energy of the public — is why Japan remains an economic cripple and why the U.S. and Europe will follow the same path into stagnation. It’s bad medicine to just treat the symptoms and ignore the disease. To solve the problem banks must write off their bad debt and be recapitalized. QE treats symptoms. Repeated liquidity infusions, according to the examples that history gives us, increase inflationary trends, shrink the public’s buying power by lessening the value of currency, and lower the standard of living. Going down this path requires ever increasing bouts of liquidity creation. The result, for the U.S. and other countries in the developed world moving in this direction, will send the national currency lower and gold, oil, and food prices much higher. The prospect is nothing less than a diminished living standard. Election Ahead — The Flim-Flam Game has Begun In June, the U.S. Government sold off some of its oil reserves — today the oil price is higher than the day after that announcement. Pure political maneuvering, we said at the time, and continue to say. We strongly believe that any such attempts to sell off stockpiles — with the aim of lowering the price of oil, food, or gold —will backfire and make the U.S. and its co-sellers look foolish. These are manipulations — flim-flam, if you will — intended to make inflation seem less than what it really is during the run-up to next year’s election. Such actions are doomed to fail. You can expect China, India, and other emerging nations to buy our stockpiles because they are trying to build their own stockpiles. It is easy to understand the psychology of the buying countries. They are growing in wealth and want to raise their standard of living. They want to protect their urban population with stockpiles in case of drought or other production problems. You can expect continued demand from the emerging world for food, energy, and gold. Speaking of which, it is interesting to note that in one single order recently, China bought more U.S. corn than the U.S. Department of Agriculture projected the Chinese would buy in all of 2011. The estimate was 500,000 metric tons for the year. The recent order was 540,000 metric tons. China’s appears to be increasing its corn stockpile in order to increase meat consumption. Cattle and other meat-producing animals are often fed on corn and soybeans. We expect China to import more corn and other food grains this year and in future years, and to greatly exceed U.S. government estimates. Please see below for a five-year corn chart.

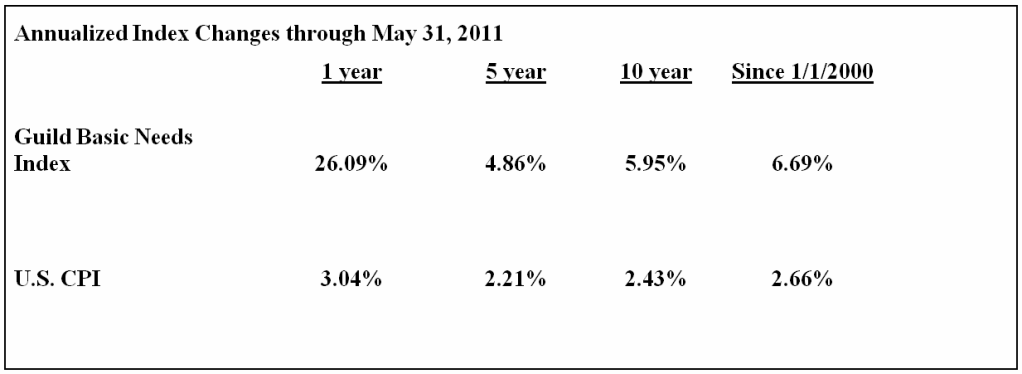

Guild Basic Needs IndexTM

Despite the fact that their policies increase inflation, governments have a tendency to understate inflation both to keep inflationary psychology from gripping the public and to avoid having to make higher payments to recipients of government payments tied to the stated inflation rate. Such payments include pensions. For these reasons, we believe that the U.S. Government understates the inflation rate in the Consumer Price Index (CPI). Because the CPI underestimates the true cost of life’s basic needs we have created the Guild Basic Needs Index to help investors and the public stay on top of their true cost of living. Wrap Up Gold, oil and food prices will rise much higher in an inflationary climate where pivotal currencies are depreciating and astronomical sums of money are being infused into sick economies. Please see our recommendation table below, and stay tuned to our upcoming letters for new recommendations. | | Date | Date | Appreciation/Depreciation | | Investment | Recommended | Closed | in U.S. Dollars | Commodity Market Recommendations | | | | | Corn | 4/20/2011 | Open | -8.1% | | Gold | 6/25/2002 | Open | +387.8% | | Oil | 2/11/2009 | Open | +172.8% | Corn | 12/31/2008 | 3/3/2011 | +81.0% | | Soybeans | 12/31/2008 | 3/3/2011 | +44.1% | | Wheat | 12/31/2008 | 3/3/2011 | +35.0% | Currency Recommendations | | | | | Short | | | | | Japanese Yen | 4/6/2011 | Open | -8.0% | | Long | | | | | Brazilian Real | 9/13/2010 | Open | +8.6% | | Long | | | | | Canadian Dollar | 9/13/2010 | Open | +7.3% | | Long | | | | | Chinese Yuan | 9/13/2010 | Open | +3.9% | | Long | | | | | Singapore Dollar | 9/13/2010 | Open | +9.8% | | Long | | | | | Swiss Franc | 9/13/2010 | Open | +24.2% | Long | | | | | Australian Dollar | 9/13/2010 | 6/29/2011 | +14.1% | | Long | | | | | Thai Baht | 9/13/2010 | 6/22/2011 | +6.5% | | Short | | | | | Japanese Yen | 9/14/2010 | 10/20/2010 | -3.3% | Equity Market Recommendations | | | | | Malaysia | 6/29/2011 | Open | +1.1% | | U.S. | 6/29/2011 | Open | -0.2% | | India | 4/6/2011 | Open | -6.0% | | Japan | 2/15/2011 | Open | -7.3% | Australia | 2/15/2011 | 6/22/2011 | -0.9% | | Canada | 3/24/2011 | 6/22/2011 | -7.1% | | Colombia | 9/13/2010 | 6/22/2011 | +2.6% | | Malaysia | 4/6/2011 | 6/22/2011 | +0.8% | | Canada | 12/16/2010 | 3/11/2011 | +7.9% | | U.S. | 9/9/2010 | 3/11/2011 | +18.1% | | South Korea | 1/6/2011 | 3/3/2011 | -2.9% | | Colombia | 9/13/2010 | 2/2/2011 | +3.9% | | China | 9/13/2010 | 1/27/2011 | +5.0% | | India | 9/13/2010 | 1/6/2011 | +7.9% | | Chile | 9/13/2010 | 12/16/2010 | +8.9% | | Indonesia | 9/13/2010 | 12/16/2010 | +9.5% | | Malaysia | 9/13/2010 | 12/16/2010 | +1.3% | | Peru | 9/13/2010 | 12/16/2010 | +32.2% | | Singapore | 9/13/2010 | 12/16/2010 | +4.8% | | Thailand | 9/13/2010 | 12/16/2010 | +11.9% | | | | | | Bond Market Recommendations | | | | | | | | | | 30 YR Long Term | | | | | U.S. Treasury Bond | 8/27/2010 | 10/20/2010 | 0.0% |

|

No comments:

Post a Comment